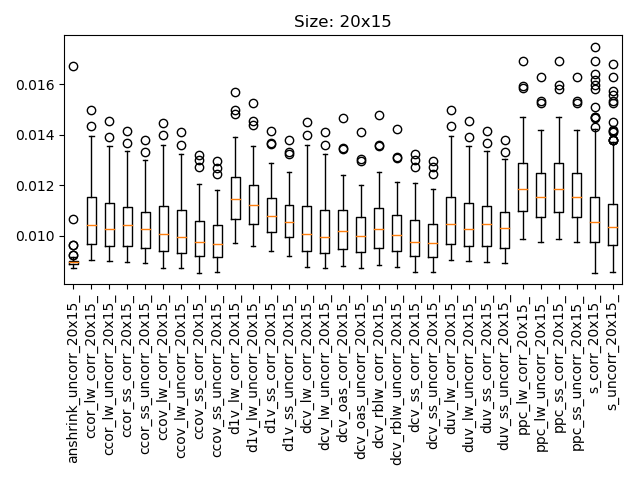

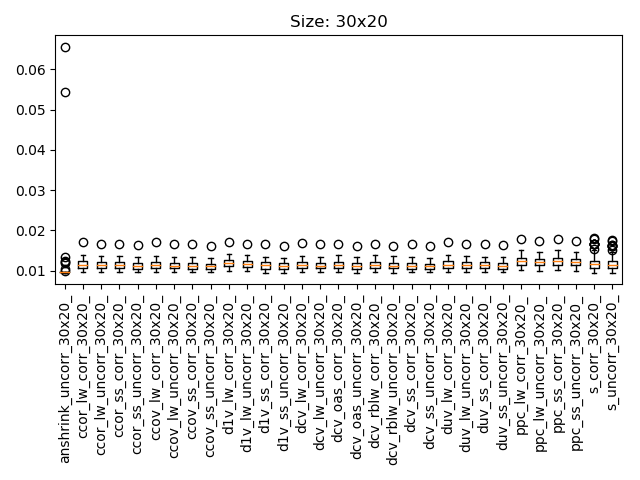

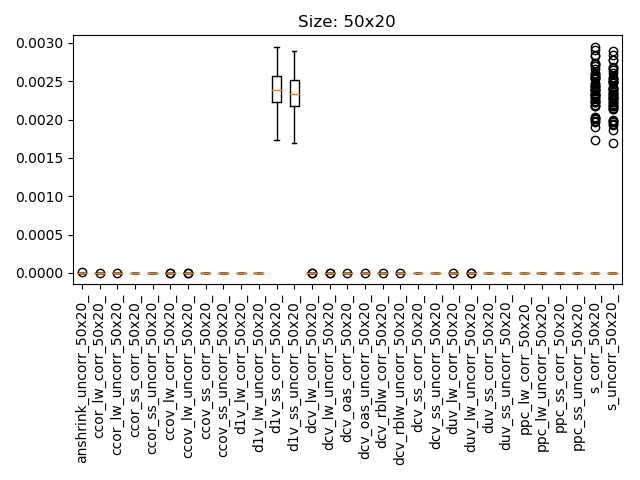

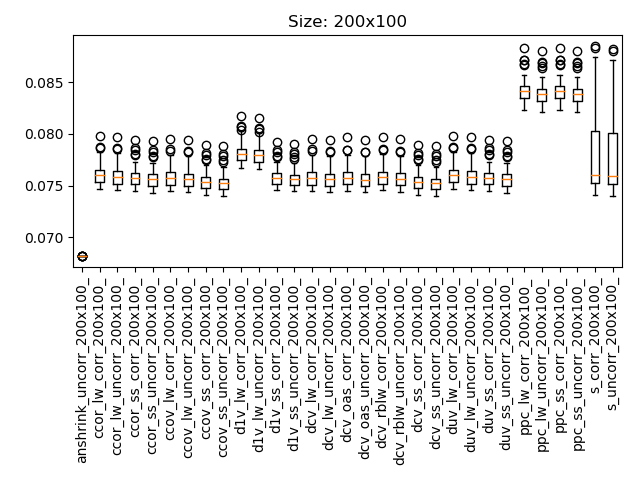

MSE Comparison

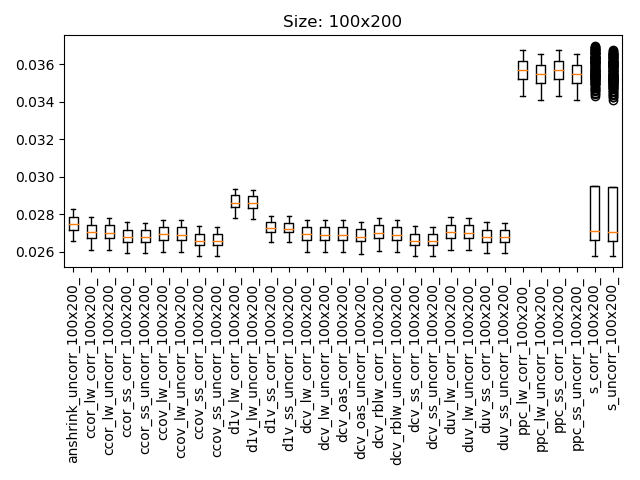

Below are results obtained with a variety of data matrices of dimensions $n\times p$. For each pair of dimension, 50 covariance matrices are generated with associated sample data matrices. The covariance obtained with the different estimators are then compared to the ground-truth and the MSE is reported.

| Abbreviation | Method |

|---|---|

anshrink | analytical nonlinear shrinkage |

ccor | LSE with constant correlation target |

ccov | LSE with constant covariance target |

d1v | LSE with identity target |

dcv | LSE with diagonal common variance target |

duv | LSE with diagonal unequal variance target |

ppc | LSE with perfect positive correlation target |

s | Simple estimator (baseline) |

_lw | uses ledoit-wolf shrinkage |

_ss | uses schaffer-strimmer shrinkage |

_oas | uses oracle approximating shrinkage |

_rblw | uses rao-blackwellised ledoit-wolf shrinkage |

Fat matrices

Tall matrices