DiffFusion.jl [∂F]

Documentation for DiffFusion.jl.

The DiffFusion.jl package implements a framework for joint simulation of financial risk factors, risk-neutral valuation of financial instruments and calculation of portfolio risk measures.

The intended purpose of the package is efficient exposure simulation for XVA and Counterparty Credit Risk (CCR).

Repository

The code for DiffFusion.jl is hosted at github.com/frame-consulting/DiffFusion.jl.

Installation

The most recent release of the package can be installed via

using Pkg; Pkg.add("DiffFusion.jl")Unit tests can be run via

Pkg.test("DiffFusion")For details on the functionality, see the Overview page.

For questions please contact info@frame-consult.de.

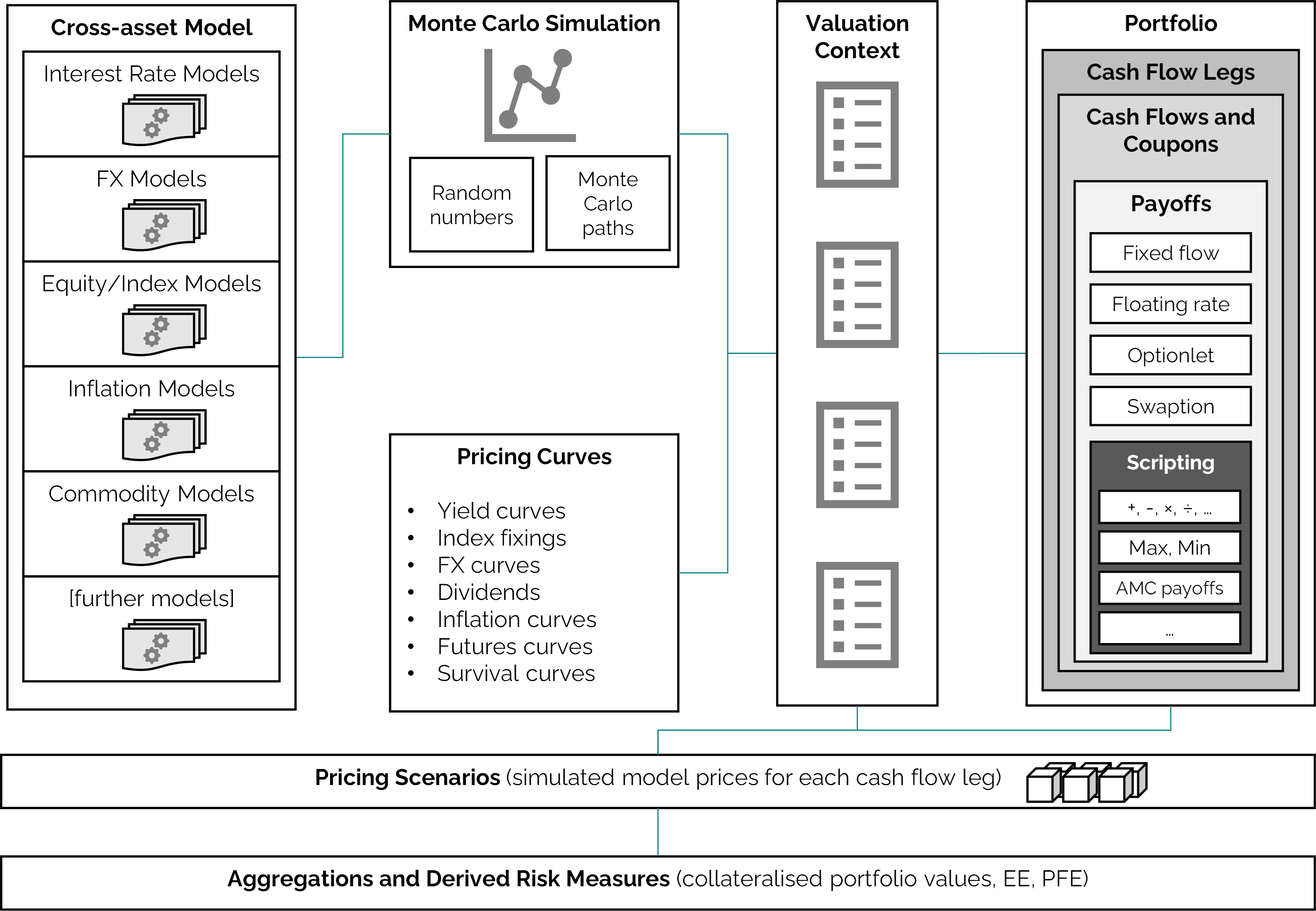

Architecture

An overview of the architecture of the framework is illustrated in below figure.

|

|---|

| Architecture of the DiffFusion.jl simulation framework. |

Details on purpose and scope are presented in the white paper DiffFusion.jl - A New Exposure Simulation Framework for the Post-Libor World.

Getting Started

Cross-asset exposure simulation can be a complex procedure. Here, we give a minimal example to illustrate the usage of the package.

For a more realistic examples, see the unit tests and component tests.

The basic usage can be decomposed into the following steps:

- model setup,

- Monte Carlo simulation,

- Monte Carlo path construction,

- financial instrument setup,

- scenario valuation.

All methods are implemented in the DiffFusion module and accessible via:

using DiffFusionModel Setup

A basic one-factor Gaussian interest rate model can be set up as follows:

δ = DiffFusion.flat_parameter(1.) # benchmark rate

χ = DiffFusion.flat_parameter( 0.01 ) # mean reversion parameter

σ = DiffFusion.flat_volatility( 0.0050 ) # short rate volatility

model = DiffFusion.gaussian_hjm_model("mdl/HJM1F", δ, χ, σ, nothing, nothing)Details on the setup of model parameters are documented in the Term Structures Functions section. Available models are documented in the Models Functions section.

Monte Carlo Simulation

Monte Carlo paths of model risk factors are stored in a Simulation object. A simulation object for our example model is calculated as follows:

ch = DiffFusion.correlation_holder("Std") # correlations for more complex models

times = 0.0:0.25:2.0 # simulation times

n_paths = 2^10 # number of simulated paths

sim = DiffFusion.simple_simulation(model, ch, times, n_paths)Further details on Monte Carlo simulation methods are documented in the Simulations Functions section.

Monte Carlo Path Construction

In order to use the Monte Carlo simulation for the pricing of financial instruments we need to specify a Path object. For the Path object we need term structures and a valuation context.

We use simple flat yield term structures for this example.

ts = [

DiffFusion.flat_forward("yc/Estr", 0.02), # discount curve

DiffFusion.flat_forward("yc/Euribor6m", 0.03), # projection curve

]More details on yield curves and model parameter term structures are documented in the Term Structures Functions section.

A context links available payoff keys with models and term structures.

ctx = DiffFusion.context(

"Std",

DiffFusion.numeraire_entry("EUR", "mdl/HJM1F", "yc/Estr"),

[

DiffFusion.rates_entry("EUR", "mdl/HJM1F",

Dict((

("ESTR", "yc/Estr"),

("EURIBOR6M", "yc/Euribor6m"),

))

),

],

)And a path combines simulation, term structures and context.

path = DiffFusion.path(sim, ts, ctx)Context and Path objects are further documented in the Monte Carlo Paths Functions section.

Financial Instrument Setup

Financial instruments are composed of cash flows (or coupons) and cash flow legs.

We use two simple floating rate coupons and one fixed rate coupon for this example.

float_coupons = [

DiffFusion.SimpleRateCoupon(

0.25, # fixing time

0.25, # start time

0.75, # end time

0.75, # pay time

0.50, # year fraction

"EUR:EURIBOR6M", # curve key

nothing, # fixing key (if index rate is already fixed)

nothing, # spread rate

),

DiffFusion.SimpleRateCoupon(

0.75, # fixing time

0.75, # start time

1.25, # end time

1.25, # pay time

0.50, # year fraction

"EUR:EURIBOR6M", # curve key

nothing, # fixing key (if index rate is already fixed)

nothing, # spread rate

),

]

fixed_coupons = [

DiffFusion.FixedRateCoupon(

1.25, # pay time

0.03, # fixed rate

1.00, # year fraction

),

]Cash flow legs add additional information to the coupons.

float_leg = DiffFusion.cashflow_leg(

"leg/1", # an alias as identifier

float_coupons,

[ 10_000.00, 10_000.00 ], # notionals

"EUR:ESTR", # curve key for discounting

nothing, # key for FX rate if applicable

-1.0, # payer leg

)

fixed_leg = DiffFusion.cashflow_leg(

"leg/2", # an alias as identifier

fixed_coupons,

[ 10_000.00 ], # notionals

"EUR:ESTR", # curve key for discounting

nothing, # key for FX rate if applicable

1.0, # receiver leg

)A financial instrument is a list of one or more cash flow legs.

More details on available cash flows and cash flow legs are documented in the Products Functions section.

Scenario Valuation

For scenario valuation we want to calculate the model price of the instrument on a set of observation times and simulated paths.

scenarios = DiffFusion.scenarios(

[ float_leg, fixed_leg ],

0.0:0.25:1.5, # observation times

path,

nothing, # no discounting to t=0

)Scenario prices are stored in a scenario cube with the dimensions

- number of paths,

- number of time steps,

- number of legs.

For our example, we can inspect the dimensions of the cube.

display(size(scenarios.X))

# Output: (1024, 7, 2)An important measure for XVA and CCR is expected (positive) exposure (EE).

Such measures can now be calculated for a given set of scenario valuation results.

using StatsBase

ee = mean(max.(sum(scenarios.X, dims=3), 0.0), dims=1)

display(ee)

# Output:

# 1×7×1 Array{Float64, 3}:

# [:, :, 1] =

# 0.0 7.98524 9.44371 147.817 148.527 0.0 0.0Scenario valuations are further documented in the Analytics Functions section.

Further Examples

The best way to become familiar with the DiffFusion framework is to have a look at the test suite.

An example for exposure simulation of a Vanilla swap portfolio is implemented in the scenario generation component test.

Individual examples on model, simulation and product setup can be found in the unit tests.